Top 5 home loan mistakes to avoid when refinancing

There has never been a better time to refinance the home loan. Interest rates are at the lowest levels we have ever seen or are likely to see in our lifetime.

It is a great idea to regularly assess your home loan to see if refinancing can save you money or provide you with additional benefits. However any home loan mistakes made while refinancing can become very costly.

When refinancing your home loan you will either switch to a new product with your current lender or move your mortgage to another bank. Refinancing provides you with a wonderful opportunity to save money, access additional features, consolidate debt or access the equity in your home.

While there are plenty of people which will readily tell you why you should refinance your home. Today we are going to look at 5 common mistakes people make when refinancing and how to avoid them.

TOP 5 HOME LOAN MISTAKES TO AVOID WHEN REFINANCING

MISTAKE #1: SHOPPING WITH 1 LENDER

Whether it’s a new car or the latest gadget, you know it pays to shop around for the best deal. When it comes to the home loan mistakes, the most common is home owners going back to the same lender that they are currently using. Why not you have had a relationship with them for years.

Each lender has only a limited number of loan products and cannot offer you true choice. For example a small difference in interest rate can have a big impact on the cost to you. On a $400,000 home loan with a 30 year term, a 0.25% difference in interest rate could cost you $59 per month, which adds up to $3,535 over the first 5 years of the loan.

Shopping around for better home refinance rates from reputable brokers is always a better alternative. Reputable finance brokers have access to many lenders and can help find a lender and product which meets your needs and requirements.

MISTAKE #2: FAILING TO SEEK OBJECTIVE INFORMATION

When questions about home loans come up, most borrowers turn to their friends, family, work colleagues, the media or their local bank. Friends, family and work colleagues are often unreliable sources of information because what has worked for one person may not be suitable for the next.

The media can be good places to get high level view of what is available, but will not shed much light on your individual situation. Banks and other lenders are good sources of information and will advise on how it suits your individual circumstances, however are limited to the products which they offer.

A reputable finance broker will provide you with information and expert advice which takes your needs and circumstances into account helping you avoid this common home loan mistake.

MISTAKE #3: NOT LEARNING ABOUT THE PROCESS

Talk to homeowners and they’ll likely tell you about how complex, confusing and time-consuming getting a home loan can be. Knowing that, it’s certainly a good idea to arm yourself with as much knowledge about borrowing as possible.

Talk to your finance broker who can educate you on the process, providing details on what is required from the application to settlement.

MISTAKE #4: FOCUSING ON IRRELEVANT MATTERS

Given that so many homeowners look to a single lender when shopping for their mortgage, it’s not surprising that most borrowers will pick lenders based on geographic proximity, a pre-existing financial relationship, or other factors, like reputation, none of which may be relevant to the loan’s total cost.

The downside of picking a lender based on location, an existing relationship or reputation is that they can lose out on getting a loan which suits your needs and requirements, resulting in long-term money going out the window.

But the best deal isn’t necessarily the lowest rate, different loan products may have the same rate but substantially different costs, which underscores the need to learn about the variety of loans available. This common home loan mistakes is easy to avoid by focusing on your needs and requirements.

MISTAKE #5: STICKING WITH THE SAME MORTGAGE ‘TIL THE END

Your home loan could become uncompetitive in only a few years. Lenders are always reassessing their interest rates and may have jacked up the rate of your loan so that it is longer competitive. The competition among lenders is such that new loan features and other innovations are being added all the time, and you might be missing out on benefits which can help you save money in the long term.

Your circumstances may have changed, a new bubbling baby on the way, the kids about to start university or parents needing your support. Whatever the reason your needs and requirements will change over time and what was a suitable loan a few short years ago may not be suitable for you now.

You should review your home loan at least every 2 years. Of all the home loan mistakes, if costs nothing to check and could save you thousands of dollars a year.

If you’re considering refinancing your home loan, your next step should be to read our Consumer’s Guide to Refinancing Your Home. In this fact-filled booklet, you’ll discover the risks and benefits of refinancing your home loan, 10 costly errors when refinancing your home, and 4 steps to hassle free refinancing of your home.

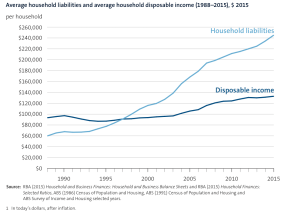

The great Australian dream is of owning your own home, but when are we going to pay off the debt. We get our dream home, but are left paying the home loan off over the next 30 years (if we are lucky).

The great Australian dream is of owning your own home, but when are we going to pay off the debt. We get our dream home, but are left paying the home loan off over the next 30 years (if we are lucky).